Rocket Companies Steering Lawsuit: CFPB Enforcement Action Explained

The Steering Trap: Why "One-Stop Shopping" is Costing You Thousands

When you’re in the middle of the most expensive purchase of your life, you want a team you can trust. You want an agent who looks out for your family and a lender who gives you the straight talk on the best rate. But for years, the industry giants have been building a "closed loop" designed to keep you from ever seeing the competition.

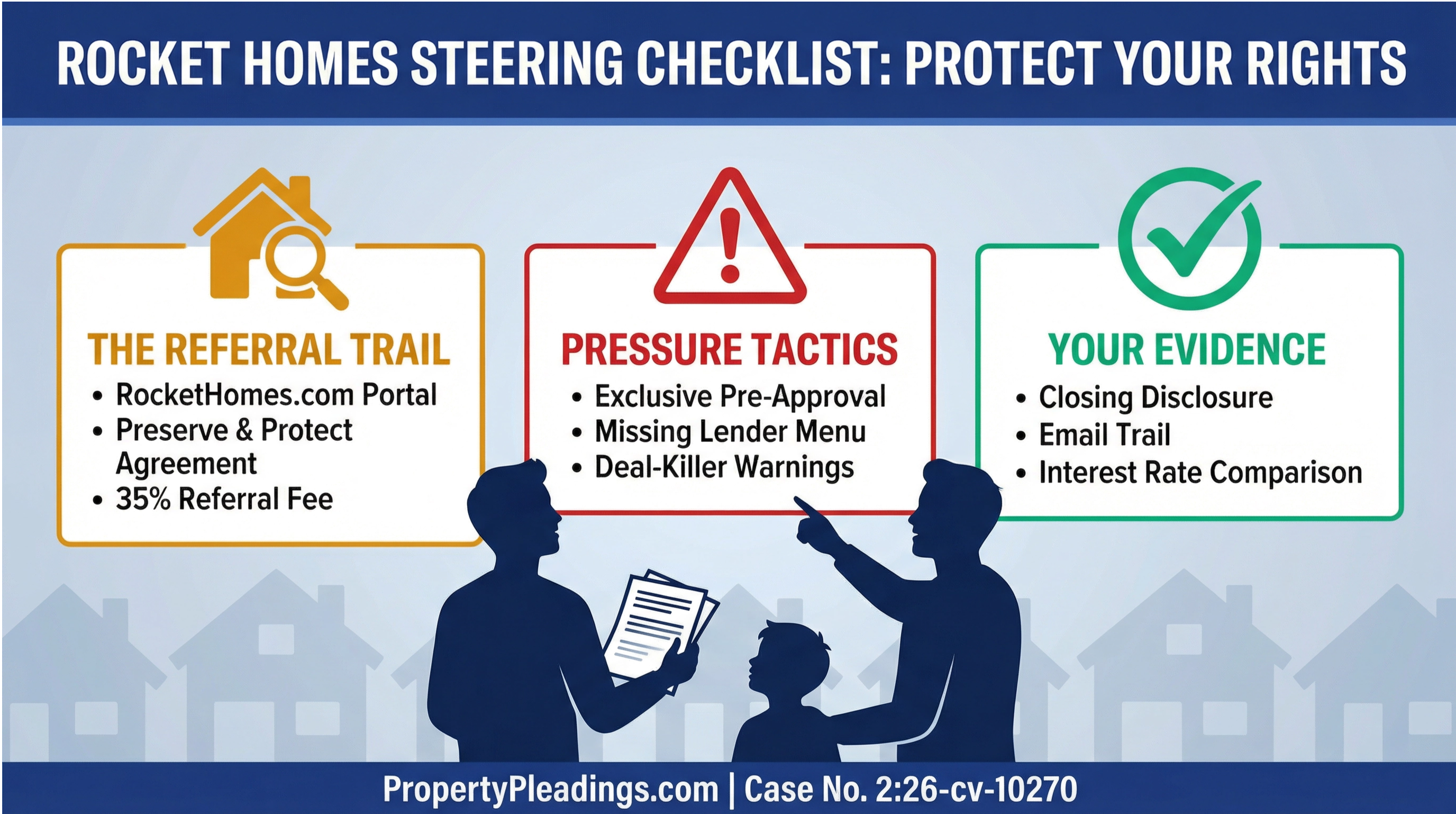

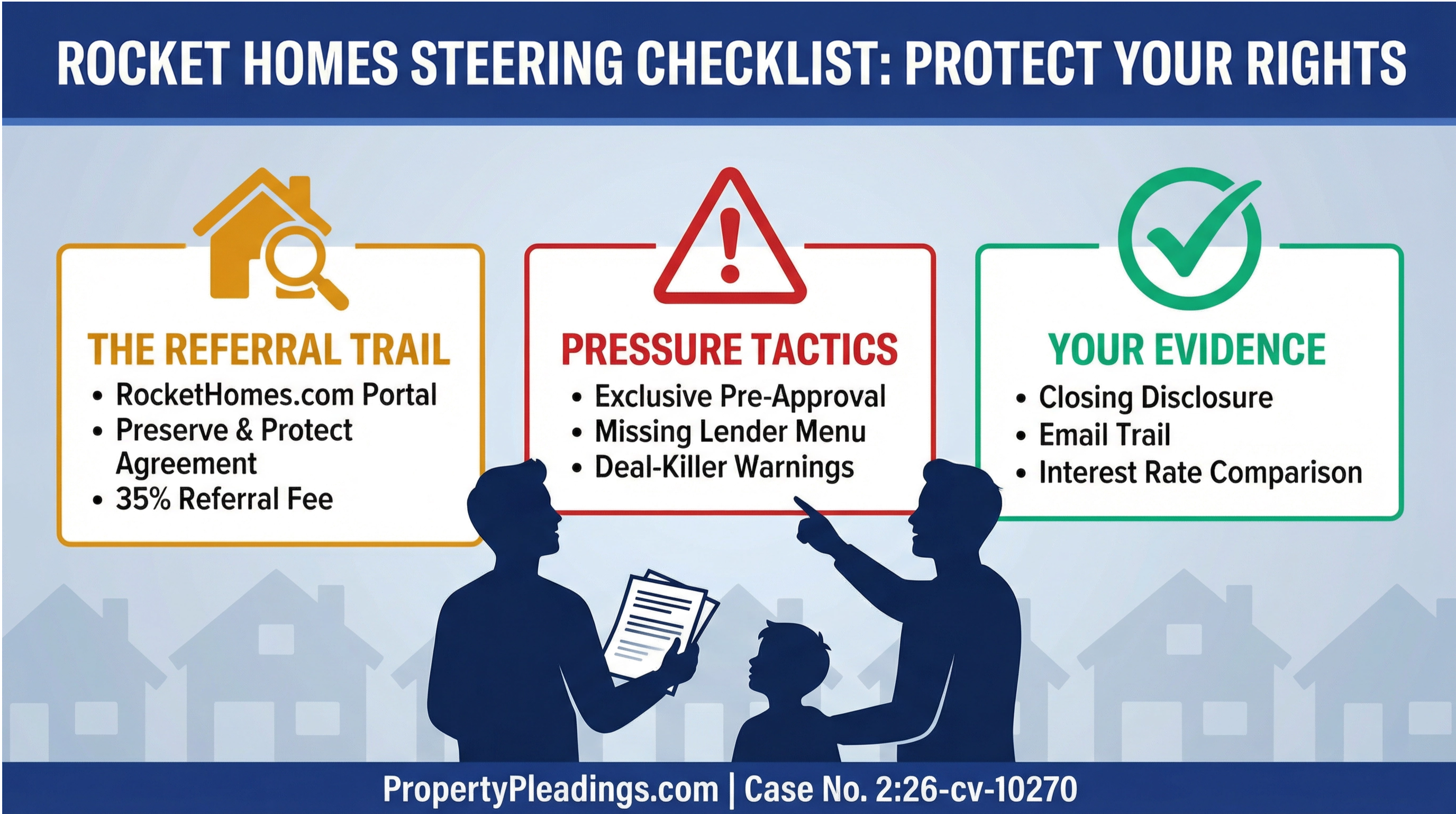

It’s a classic "tricks and traps" scenario. In late 2024, the CFPB pulled back the curtain on what they called an illegal kickback scheme—alleging that Rocket Homes was essentially "steering" families into Rocket Mortgages. They didn't do it with a wink and a nod; they did it with structural pressure, allegedly rewarding agents with "Dog Bone" gift cards and future leads only if they kept clients within the Rocket ecosystem.

Now, the big banks and the lobbyists will tell you this is just "convenience." They’ll say that putting your brokerage, your lender, and your title company under one roof is the "future." But I’ve got a plan to show you the real cost of that convenience.

Even though the government’s 2024 lawsuit was dismissed during the 2025 deregulatory wave, the people are persisting. A massive new class-action lawsuit filed in January 2026 is holding Rocket to account for the hundreds of thousands of homeowners who were allegedly steered into higher-interest, "substandard" loans.

We’re not just talking about a few dollars here; we’re talking about the difference between a fair market and a rigged one. Because at the end of the day, a market where you’re not allowed to shop around isn't a market at all—it's a trap.

And we are going to help you find the way out.

The real estate industry is currently navigating a period of unprecedented legal scrutiny and transformative change. From landmark antitrust settlements challenging long-standing commission rules to a renewed focus on consumer protection, every corner of the market is feeling the pressure. Amidst this swirling landscape, a significant development is on the horizon: a looming CFPB enforcement action against Rocket Companies, expected in December 2024. This action targets alleged "steering" practices, a term that carries profound implications for both consumers and professionals.

For years, Rocket Mortgage, a subsidiary of Rocket Companies, has been a dominant force in the mortgage lending space, known for its innovative technology and aggressive marketing. However, with great market share comes great responsibility, and regulatory bodies like the Consumer Financial Protection Bureau (CFPB) are increasingly vigilant about ensuring fair and transparent practices. This blog post will delve into the specifics of the anticipated Rocket Mortgage lawsuit, explain what "real estate steering" entails, and explore the broader context of CFPB enforcement in the real estate and mortgage sectors. Understanding these dynamics is crucial for anyone involved in buying, selling, or financing a home.

The CFPB and its Role in Consumer Protection

The Consumer Financial Protection Bureau (CFPB) was established in the wake of the 2008 financial crisis with a clear mandate: to protect consumers in the financial marketplace. This independent agency is responsible for regulating a wide array of financial products and services, including mortgages, credit cards, and student loans. Its powers are extensive, encompassing rulemaking, supervision, and enforcement actions against companies that violate federal consumer financial laws.

When the CFPB initiates an enforcement action, it typically means the agency has identified practices it believes are unfair, deceptive, or abusive, or that violate specific statutes like the Real Estate Settlement Procedures Act (RESPA). These actions can result in significant penalties, including fines, restitution to consumers, and mandates for companies to change their business practices. The anticipated CFPB enforcement against Rocket Companies underscores the agency's commitment to policing the mortgage industry and ensuring a level playing field for consumers.

Understanding Real Estate Steering

At the heart of the anticipated Rocket Mortgage lawsuit is the allegation of "real estate steering." But what exactly does this term mean, and why is it problematic?

Real estate steering, in the context of mortgage lending, refers to practices where a real estate agent, broker, or lender improperly influences a consumer's choice of service providers (e.g., a specific mortgage lender, title company, or inspector) for their own financial benefit, rather than acting solely in the consumer's best interest. This can manifest in several ways:

Exclusive Referrals: An agent consistently recommends only one mortgage lender, even if other lenders might offer better terms or rates for the client.

Conditional Services: A lender or agent implies that using a particular service provider is required to receive preferential treatment or even to close the deal.

Hidden Kickbacks or Referral Fees: While RESPA generally prohibits unearned fees and kickbacks for referrals, sophisticated arrangements can sometimes skirt these rules, creating incentives for steering.

Discouraging Alternatives: Actively dissuading a client from exploring other options or comparing offers from different providers.

The core issue with steering is that it undermines consumer choice and can lead to consumers paying higher costs, receiving less favorable terms, or missing out on better options that would genuinely serve their needs. It creates a conflict of interest, where the professional's financial gain takes precedence over the client's welfare. This is precisely why the CFPB and other regulatory bodies view it as a serious violation of consumer protection principles.

The Rocket Companies CFPB Enforcement Action: What We Know

While the specific details of the CFPB enforcement action against Rocket Companies are not yet fully public, the expectation of its arrival in December 2024 signals a significant regulatory focus. Industry observers and legal experts anticipate that the action will likely center on allegations related to steering practices, potentially involving how Rocket Mortgage interacts with real estate agents and brokers, or how it promotes its own services in conjunction with other Rocket Companies entities.

Rocket Companies operates a diverse portfolio of businesses, including Rocket Mortgage (mortgage lending), Rocket Homes (real estate brokerage and search portal), and Rocket Title (title services), among others. This integrated structure, while offering convenience, also presents potential challenges regarding perceived or actual steering. The CFPB will likely scrutinize whether Rocket's various entities have engaged in practices that unfairly direct consumers towards Rocket-affiliated services, potentially limiting consumer choice and competition.

The timing of this enforcement action is also noteworthy. It comes at a time when the entire real estate industry is under a microscope, with major antitrust lawsuits challenging traditional commission structures and a heightened awareness of consumer costs. The CFPB's action against a prominent player like Rocket Companies sends a clear message that regulatory oversight of consumer financial services remains robust and that companies must prioritize transparency and fair dealing.

Potential Impact of the Rocket Mortgage Lawsuit

A CFPB enforcement action against a company of Rocket's size and influence could have far-reaching consequences:

Financial Penalties: Significant fines and restitution payments to affected consumers are common outcomes of CFPB actions.

Operational Changes: Rocket Companies may be compelled to revise its business practices, referral agreements, and internal compliance protocols to prevent future steering.

Reputational Damage: Public enforcement actions can impact consumer trust and brand perception.

Industry-Wide Scrutiny: This action could prompt other mortgage lenders and integrated real estate companies to review their own referral and marketing practices to ensure compliance.

Increased Transparency: Ultimately, the goal is to foster greater transparency and empower consumers to make informed choices without undue influence.

Broader Context: Anti-Steering and Antitrust in Real Estate

The Rocket Mortgage lawsuit and the focus on steering are not isolated incidents. They are part of a larger trend of increased regulatory and legal scrutiny across the real estate sector. The challenges to the buyer broker commission rule, exemplified by the NAR Settlement ($418M, final approval February 6, 2026) and settlements from major brokerages like Anywhere ($83.5M), RE/MAX ($55M), HomeServices of America ($250M), and Keller Williams ($70M), all stem from allegations of anticompetitive practices and a lack of transparency for consumers.

These cases, often citing violations of the Sherman Antitrust Act, argue that traditional rules have inflated commission costs and limited consumer choice. While the Rocket Companies action specifically targets steering in the mortgage context, the underlying principle is similar: ensuring fair competition and protecting consumers from practices that limit their options or increase their costs without justification.

The upcoming MLS rule changes effective August 2024, which will prohibit listing agents from offering buyer broker compensation through the MLS, are a direct outcome of these antitrust challenges. These changes are designed to unbundle services, make compensation more transparent, and encourage direct negotiation between buyers and their agents. In this new landscape, the potential for steering, whether by agents or lenders, becomes even more critical to monitor, as consumers will be directly responsible for understanding and negotiating their agent's fees.

The Importance of Buyer-Broker Agreements

In this evolving environment, buyer-broker agreement requirements are becoming paramount. These agreements, which outline the services an agent will provide, the duration of the representation, and the compensation structure, are vital for consumer protection. They ensure transparency and clarify the professional relationship, helping to mitigate the risks of steering. As the industry shifts, robust buyer-broker agreements will serve as a crucial safeguard, empowering buyers and holding agents accountable.

What This Means for Consumers and Professionals

For Consumers:

Empowerment Through Information: The increased scrutiny on steering and commission practices means consumers will have more information and more control over their real estate transactions.

Shop Around: It is more critical than ever to compare multiple mortgage lenders, real estate agents, and other service providers. Don't feel pressured to use a recommended provider without doing your own research.

Ask Questions: Inquire about referral relationships, compensation structures, and why a particular provider is being recommended.

Understand Agreements: Carefully read and understand all agreements, especially buyer-broker agreement requirements and mortgage disclosures.

Report Concerns: If you suspect steering or unfair practices, you can report them to the CFPB or other relevant regulatory bodies.

For Real Estate and Mortgage Professionals:

Review Compliance: It's imperative to review all referral arrangements, marketing practices, and internal policies to ensure strict compliance with RESPA and anti-steering regulations.

Transparency is Key: Be upfront and transparent with clients about all potential service providers, their options, and any referral relationships you may have (though direct referral fees are generally prohibited under RESPA).

Focus on Best Interests: Always prioritize the client's best interests over any potential financial gain from a specific referral.

Adapt to Changes: Stay informed about the MLS rule changes effective August 2024 and the evolving legal landscape. Proactively adapt your business practices to align with new requirements and consumer expectations.

Educate Clients: Help clients understand their choices, the importance of shopping around, and the value of a strong buyer-broker agreement.

Looking Ahead: The Future of Real Estate Transactions

The anticipated CFPB enforcement action against Rocket Companies is another significant piece in the complex puzzle of real estate reform. Coupled with the NAR Settlement and other brokerage settlements, it signals a clear shift towards greater consumer protection, transparency, and competition. The industry is moving towards a model where consumers are more empowered to choose their service providers and negotiate fees, rather than relying on opaque, bundled services.

While these changes may present challenges for some industry players, they ultimately aim to create a more equitable and efficient market for everyone. The focus on eliminating steering and promoting fair practices will benefit consumers by ensuring they receive the best possible advice and services tailored to their individual needs, free from conflicts of interest.

The December 2024 timeframe for the Rocket Companies action will be a critical moment, providing more clarity on the specific allegations and the CFPB's stance on integrated real estate services. We will continue to monitor this and other developments closely, providing timely updates and analysis on Real Estate Lawsuit Tracker.

Stay Informed and Protect Your Interests

The legal landscape of real estate is changing rapidly. Whether you are a consumer buying or selling a home, or a professional navigating these new rules, staying informed is paramount. The Real Estate Lawsuit Tracker is your comprehensive resource for understanding these complex issues.

Explore our resources to learn more:

Real Estate Lawsuits & Settlements: Get a complete overview of all ongoing and settled cases affecting the industry.

Settlement Checker: Determine if you are eligible for compensation from any of the major settlements.

Attorney Directory: Find legal professionals specializing in real estate law to guide you through these changes.

Document Library: Access key legal documents, court filings, and regulatory guidelines.

Impact Calculator: Understand how these changes might affect your specific real estate transaction.

Don't be caught off guard by the evolving real estate market. Empower yourself with knowledge and ensure your interests are protected.

Copyright © 2026 Real Estate Lawsuit Tracker. All rights reserved.

_Share this post

About the Author

Frances Flynn Thorsen

REALTOR® • Writer • Educator • Consumer Advocate

Frances Flynn Thorsen brings nearly 40 years of frontline experience in residential real estate, with a career built at the intersection of consumer advocacy, market literacy, and professional accountability. A leading REALTOR®, writer, educator, and trusted advisor to high-performing agents, she translates complex market forces and industry practices into clear, practical guidance for consumers and the professionals who serve them.

eXp Realty LLC • State College, PA • License RS148436A

Related Articles