What Documents Do I Need to File a Settlement Claim?

The Paper Trail to Justice: Why Your "Fine Print" is the Key to Fighting Back

When you sit down at your kitchen table to look over the paperwork from your last home sale, it can feel like you’re staring at a 3,000-piece puzzle where half the pieces are missing. For decades, the big brokerage firms and the powerful interest groups have banked on that feeling. They’ve relied on a "wiring diagram" of real estate commissions so complex and so buried in legalese that most families just sign on the dotted line and hope for the best.

Think about it this way: If you bought a toaster today that had a one-in-five chance of bursting into flames and burning your house down, we wouldn't blame you for not reading the 31-page manual to find the faulty wiring diagram on page 25. We’d say the toaster was rigged to fail.

For years, the real estate market has been that exploding toaster. The "cooperative compensation" rules were a structural trap designed to siphoned off your home equity before you even had a chance to negotiate. But here’s the thing: The evidence of that rig is sitting in your filing cabinet right now.

Those "boring" documents—your Closing Disclosure, your HUD-1, your old sales contracts—aren't just paper. They are the receipts for a system that was weighted against you. As we move into this final wave of settlements in February 2026, those documents are your best tools to demand accountability.

I’ve got a plan to help you gather that evidence. We’re going to cut through the jargon, find the "tricks and traps" in your old files, and make sure you have everything you need to stand up and say: the system was rigged, and I’m here to get my fair share back.

We’ve done it before, and together, we’re doing it again.

The landscape of real estate commissions is undergoing a monumental shift, driven by a series of landmark antitrust lawsuits. These legal challenges, primarily targeting the long-standing practice of seller-paid buyer broker commissions, have culminated in significant settlements from major industry players like the National Association of REALTORS® (NAR), Anywhere Real Estate, RE/MAX, HomeServices of America, and Keller Williams. For many homebuyers and sellers who transacted during the class periods, these settlements represent an opportunity for financial recovery.

However, navigating the claims process can seem daunting. A crucial first step is understanding what documentation you'll need to substantiate your claim. This comprehensive guide will walk you through the essential documents required to file a real estate settlement claim, ensuring you're prepared to seek the compensation you may be entitled to. We'll delve into the specifics of what constitutes valid proof, why these documents are important, and how to gather them effectively.

Understanding the Real Estate Settlement Landscape

Before diving into documentation, it's vital to grasp the context of these settlements. The core of these lawsuits, often citing violations of the Sherman Antitrust Act, challenged the rules that allegedly inflated buyer broker commissions. The most prominent of these is the NAR Settlement, which, with its final approval set for February 6, 2026, includes a substantial $418 million fund. Other significant settlements include:

Anywhere Real Estate (parent company of Coldwell Banker, Century 21, Sotheby's): $83.5 million

RE/MAX: $55 million

HomeServices of America (a Berkshire Hathaway affiliate): $250 million

Keller Williams: $70 million

Multi-firm settlements: William Raveis ($4.1 million), Howard Hanna ($32 million), EXIT Realty ($1.5 million), Windermere, and Lyon.

These settlements aim to provide restitution to eligible class members – typically individuals who paid a buyer broker commission during a specific timeframe. The exact eligibility criteria, class periods, and claims processes vary by settlement, underscoring the importance of verifying your specific situation using tools like our Settlement Checker.

Why Documentation is Paramount for Your Claim

Filing a successful settlement claim hinges on providing clear, verifiable evidence of your transaction and the associated costs. Claim administrators require documentation to:

Verify Eligibility: Confirm you were a party to a qualifying real estate transaction within the specified class period.

Substantiate Damages: Prove the amount of buyer broker commission you paid or were charged.

Prevent Fraud: Ensure the integrity of the claims process and distribute funds fairly to legitimate claimants.

Without proper documentation, your claim may be delayed, rejected, or result in a lower payout than you are entitled to. Therefore, gathering all relevant real estate settlement claim documents is the most critical step.

Essential Documents for Your Real Estate Settlement Claim

While the specific requirements might vary slightly between settlements, a core set of documents will almost universally be needed. Think of these as your "proof of purchase" for the services rendered by a buyer's agent. Here’s a detailed breakdown:

1. Proof of Home Purchase or Sale Transaction

This is the foundational document. You need to demonstrate that you bought or sold a home during the relevant class period. Key documents include:

Closing Disclosure (CD) or HUD-1 Settlement Statement: This is arguably the most important document. It details all financial aspects of your real estate transaction, including purchase price, loan amounts, and, crucially, all fees and commissions paid. Look for lines itemizing commissions paid to both the seller's agent and the buyer's agent. This document serves as primary proof of home purchase for settlement purposes.

Sales Contract / Purchase Agreement: This legally binding document outlines the terms and conditions of your home purchase or sale. It will confirm the transaction date, property address, and often include initial agreements regarding commission structures.

Deed: The legal document transferring ownership of the property. While it doesn't detail commissions, it confirms the transaction and your ownership.

Escrow Instructions: These documents provide directives to the escrow agent regarding the handling of funds and documents during the closing process, often referencing commission payments.

Tip: If you can't locate your Closing Disclosure or HUD-1, try contacting the real estate agent, title company, or attorney who handled your closing. They often retain records for several years.

2. Evidence of Commission Payment

This category is critical for demonstrating the financial impact on you. The goal is to show that a buyer broker commission was paid as part of your transaction.

Closing Disclosure (CD) or HUD-1 Settlement Statement (Revisited): As mentioned, these documents explicitly list commission payments. On a HUD-1, you might find these under sections like "800. Items Payable in Connection With Loan" or "1100. Title Charges." On a Closing Disclosure, look for sections related to "Other Costs" or "Commissions." The key is to identify the line item showing the buyer's agent commission, even if paid by the seller.

Commission Agreements: If you signed a separate agreement with your buyer's agent detailing their commission structure, this would be valuable. This could be a Buyer-Broker Agreement, which specifies the agent's compensation, services, and the duration of the agreement. While these were not universally required in the past, they are becoming standard practice due to the MLS rule changes effective August 2024, which mandate written buyer-broker agreements.

Invoices or Receipts: Less common for commissions paid at closing, but if you paid any portion of your buyer's agent commission directly out-of-pocket, retain any invoices or receipts.

Important Note on "Seller-Paid" Commissions: Even if your Closing Disclosure states the commission was "paid by seller," you may still be eligible. The lawsuits argue that these costs were effectively passed on to the buyer through a higher purchase price, or that sellers were compelled to offer them to ensure their homes were shown. The focus is on whether a buyer broker commission was paid as part of the transaction, regardless of the direct payer listed on the closing statement.

3. Identification and Contact Information

Standard for any claim, you'll need to provide:

Government-Issued ID: A driver's license or passport to verify your identity.

Current Contact Information: Your mailing address, email address, and phone number to receive communications regarding your claim.

Social Security Number (SSN) or Taxpayer Identification Number (TIN): Often required for tax purposes if the settlement payment exceeds a certain threshold.

4. Transaction-Specific Details

Be prepared to provide specific information about your transaction, even if not explicitly a document:

Property Address: The full address of the home bought or sold.

Transaction Date: The closing date of the purchase or sale.

Names of Parties Involved: Your name(s), and potentially the names of the real estate agents and brokerage firms involved.

Purchase Price: The final sale price of the property.

Where to Find Your Documents

Gathering these documents might require a bit of detective work, especially for older transactions. Here are common sources:

Your Personal Records: Check any physical or digital files you keep related to your home purchase or sale.

Real Estate Agent: Your former real estate agent (both buyer's and seller's) may have copies of the sales contract, commission agreements, and even the Closing Disclosure.

Title Company or Escrow Company: These entities are legally required to retain closing documents for a significant period. Reach out to the company that handled your closing.

Lender: Your mortgage lender will have copies of the Closing Disclosure and other loan-related documents.

Real Estate Attorney: If you used an attorney for your closing, they would have a complete file of all transaction documents.

County Recorder's Office: The deed is a public record and can be obtained from your local county recorder or clerk's office.

Navigating Specific Settlement Requirements and Key Concepts

While the general document list applies, remember that each settlement has its own nuances. For instance, the NAR Settlement is distinct from the individual brokerage settlements. Some settlements might have different class periods or specific definitions of who qualifies. It's crucial to consult the official settlement websites or our Settlement Checker for precise details.

The Impact of MLS Rule Changes and Buyer-Broker Agreements

The upcoming MLS rule changes effective August 2024, stemming from the NAR Settlement, will significantly alter how buyer agent compensation is handled. The rule prohibiting listing agents from offering compensation to buyer brokers via the MLS will likely lead to more direct negotiations and, importantly, a greater emphasis on written buyer-broker agreement requirements. While these changes are forward-looking, if you have a buyer-broker agreement from a past transaction, it will be a valuable document for your claim, as it directly addresses commission. These changes also aim to address concerns about "steering practices," where agents might have prioritized properties offering higher commissions.

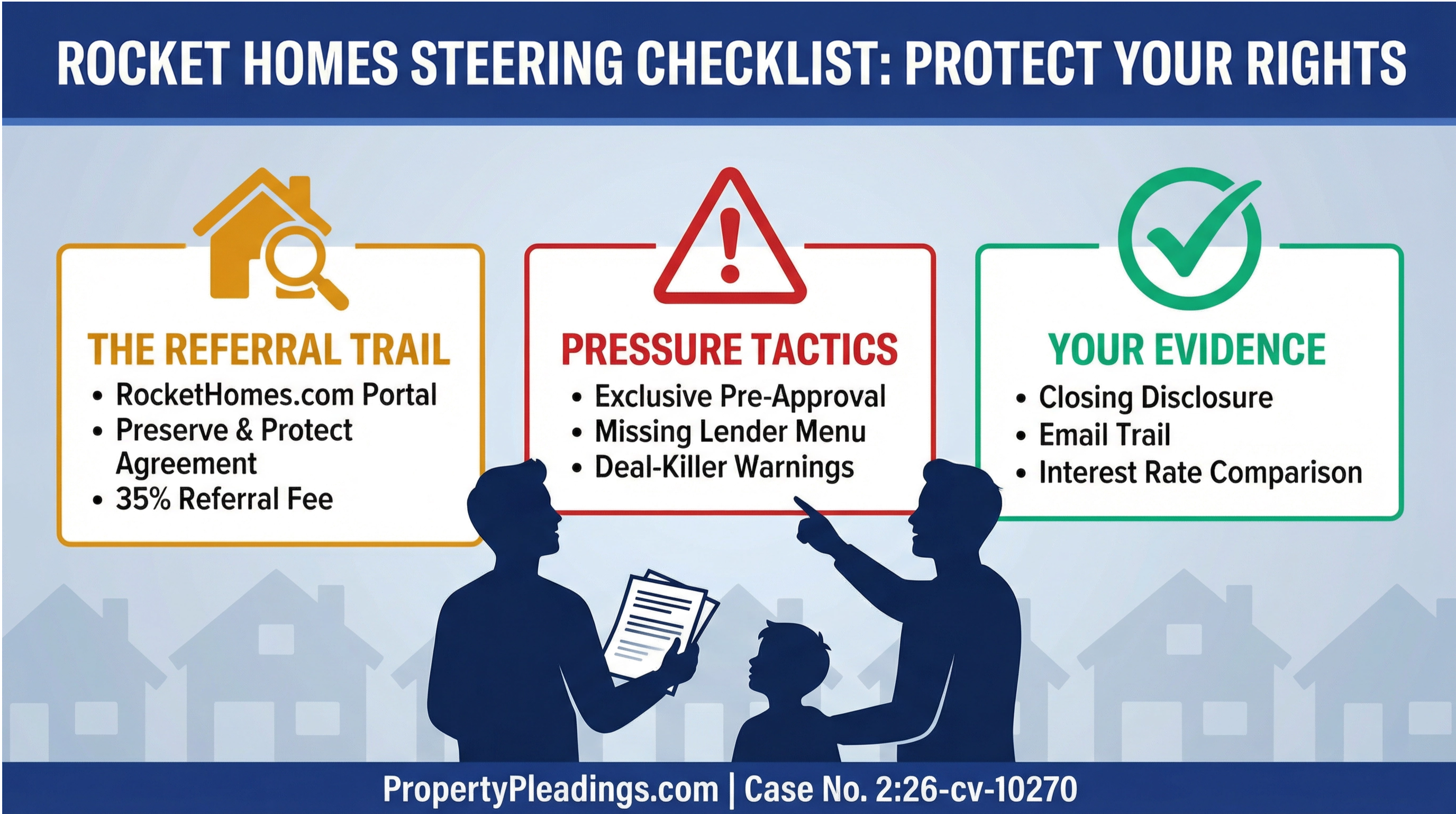

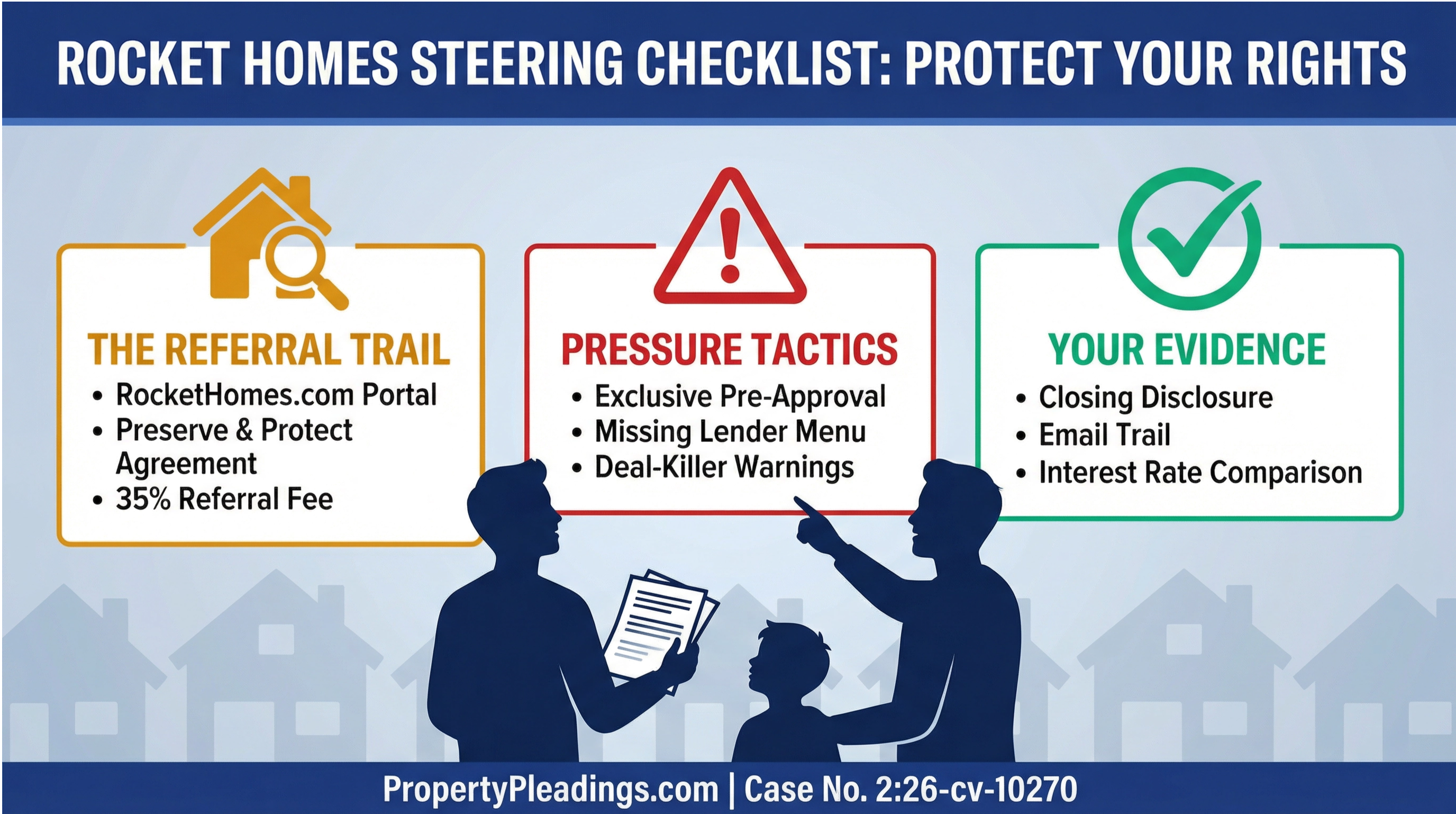

Future Considerations: Rocket Companies and Other Actions

It's also important to stay informed about ongoing legal developments. For example, Rocket Companies faces a CFPB enforcement action in December 2024, which, while different in nature, highlights the continued scrutiny on real estate and mortgage industry practices. This underscores the dynamic nature of real estate law and the potential for future claims or changes.

Preparing Your Claim: A Step-by-Step Approach

Identify Relevant Settlements: Use our Settlement Checker to determine which settlements you might be eligible for based on your transaction dates and the brokerage firms involved.

Gather All Potential Documents: Start collecting every document related to your home purchase or sale within the relevant class periods. Dig through old files, contact past agents, title companies, and lenders.

Organize and Review: Create a digital folder for each transaction. Label documents clearly (e.g., "Closing Disclosure - 123 Main St - 2019"). Highlight or mark the sections pertaining to commissions.

Check Eligibility Criteria: Carefully read the eligibility requirements for each settlement you believe you qualify for. Ensure your documents directly address these criteria.

Complete the Claim Form: Once the claims process opens for a specific settlement, fill out the official claim form accurately. Attach your organized documentation as requested.

Keep Copies: Always retain copies of everything you submit.

Seek Professional Advice: If you encounter difficulties or have complex circumstances, consider consulting with an attorney specializing in real estate law. Our Attorney Directory can help you find qualified professionals.

Conclusion: Your Path to Recovery

The real estate settlement claims represent a significant opportunity for consumers to recoup funds from past transactions. While the process requires diligence in gathering documentation, the effort can be well worth it. By meticulously collecting your real estate settlement claim documents, especially your proof of home purchase for settlement through Closing Disclosures or HUD-1 statements, you position yourself for a successful claim.

Stay informed, be thorough, and utilize the resources available on Real Estate Lawsuit Tracker to navigate this evolving landscape. Your proactive approach to documentation is the key to unlocking potential compensation.

Ready to Check Your Eligibility?

Don't miss out on potential compensation. Use our tools to understand your rights and prepare your claim.

Image Credit: Nano Banana

_Share this post

About the Author

Frances Flynn Thorsen

REALTOR® • Writer • Educator • Consumer Advocate

Frances Flynn Thorsen brings nearly 40 years of frontline experience in residential real estate, with a career built at the intersection of consumer advocacy, market literacy, and professional accountability. A leading REALTOR®, writer, educator, and trusted advisor to high-performing agents, she translates complex market forces and industry practices into clear, practical guidance for consumers and the professionals who serve them.

eXp Realty LLC • State College, PA • License RS148436A

Related Articles